In the labyrinth of the 21st-century economy, achieving financial independence has become a quest of paramount importance. It’s more than just a numerical game—it’s a pathway to freedom, to stability, and to choices that enable the life we dream of.

In a world where monetary health impacts every facet of our lives—from the roofs over our heads to the food on our plates—maintaining command over our finances is not just advisable, it’s essential.

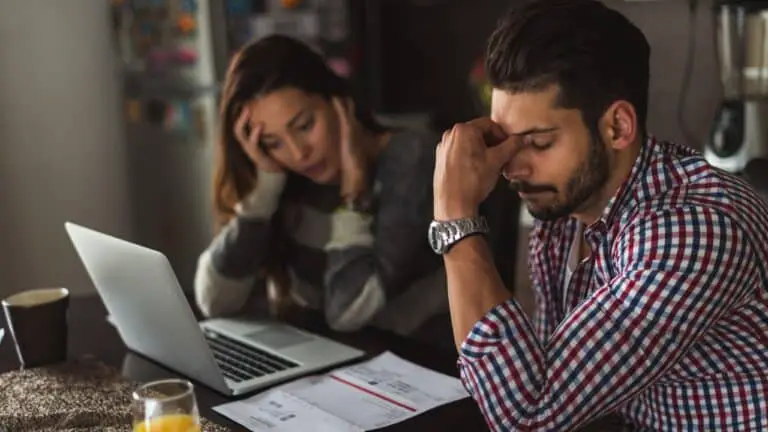

That said, debt can be the ‘minotaur’ in this economic maze, holding us captive in a cycle that often seems inescapable. It lurks in the corners of higher education loans, nestles in the crevices of credit card statements, and hides in the shadows of mortgage payments. But fear not, for breaking free from these chains before the third decade of life isn’t a Herculean feat—it’s a mission entirely possible with the right guidance.

That’s where this article comes into play. We present you with a roadmap of four pivotal rules, each designed to guide you out of the labyrinth of debt and into the sunlit realm of financial liberation—all by the age of 30. So gear up for an enlightening journey to seize control of your financial destiny, creating a future where your dreams aren’t mortgaged, but funded. Let’s turn that page and delve into the world of debt-free living.

Rule 1: Cultivate a Healthy Relationship With Money

Money and humans share a nuanced relationship, painted with strokes of necessity, desire, and often, anxiety. To master the art of becoming debt-free, the first rule necessitates a reformation of this relationship.

Understanding Money: A Tool, Not a Solution

Money, contrary to many misconceptions, is not a panacea for life’s challenges. Instead, envision it as a means to an end, a tool that can construct or dismantle your financial health.

Money is a facilitator—it aids in fulfilling your needs, wants, and dreams. However, it’s not a magic wand that can instantly solve problems or create happiness. Once you understand this crucial distinction, you pave the way towards using money more strategically, focusing on wealth creation rather than wealth consumption.

Implementing Budgeting: Your Financial Compass

If understanding money is the ship to financial independence, then budgeting is the compass guiding that ship. Without it, you’re at the mercy of unanticipated expenditures and impulsive buys—a quick route to debt accumulation.

Budgeting is akin to charting your financial course. It entails documenting income and expenses, identifying non-negotiable costs (rent, utilities), and determining discretionary spending (entertainment, dining out). This exercise imparts a clear picture of where your money comes from, where it goes, and how much of it can be steered towards debt elimination.

A budget doesn’t restrict freedom; it creates it. It equips you to live within your means, avoiding the pitfalls of overspending and under-saving. By adhering to a budget, you not only control your money, but you also reclaim control of your life from the clutches of debt.

Implementing these two aspects of Rule 1 forms a solid foundation for your debt-free journey. Now, let’s navigate forward, embracing the art of prioritizing debt repayment.

Rule 2: Prioritize Debt Repayment

Embarking on the journey to debt-freedom demands that we understand and address the burden we’re seeking to eliminate. It’s not just about paying off what we owe, but comprehending the profound impact debt has on our lives and exploring strategies to tackle it head-on.

The Impact of Debt: More Than Just Numbers

Debt is not just an economic constraint—it’s an invisible shackle that can cast long shadows on mental well-being. The burden of owing money often brings with it a whirlwind of stress, anxiety, and feelings of uncertainty, impacting not only personal happiness but also professional productivity and relationships.

Financially, carrying debt translates to the constant outflow of money towards interest payments, reducing the resources available for other essential areas such as savings, investments, or experiences that enrich life. It hinders the growth of your wealth and limits your financial flexibility. Acknowledging these impacts is the first step in understanding why debt repayment should be a priority.

Debt Repayment Strategies: Snowball and Avalanche

There’s no one-size-fits-all strategy for debt repayment—it largely depends on personal circumstances and psychological comfort. However, two well-recognized techniques can act as your starting points: the ‘Snowball Method’ and the ‘Avalanche Method.’

The Snowball Method emphasizes motivation. Start by paying off the smallest debts while maintaining minimum payments on larger ones. Each debt paid off fuels a sense of achievement, keeping you motivated on your debt-free journey.

The Avalanche Method, on the other hand, is all about math. You begin by paying off the debt with the highest interest rate while maintaining minimum payments on the rest. This method saves you the most money over time, as it curbs the amount you shell out in interest.

Choosing between the two is a matter of personal preference—some find the quick wins in the Snowball Method motivating, while others prefer the long-term savings offered by the Avalanche Method. The key is to select a strategy that you can stick to consistently, inching closer to a debt-free life with every payment.

The roadmap is taking shape: understanding money, implementing budgeting, and prioritizing debt repayment. But what’s next on our route to becoming debt-free by 30? Let’s delve into Rule 3.

Rule 3: Build and Maintain an Emergency Fund

As we journey towards financial independence, we can’t underestimate the importance of preparing for the unexpected.

Life, with its twists and turns, can throw us a financial curveball when we least expect it. This is where the safety net of an emergency fund comes into play.

Why an Emergency Fund: Financial Parachute in a Freefall

An emergency fund is more than just a component of a well-rounded financial plan—it’s a lifeline. It’s the financial buffer that stands between you and life’s uncertainties, whether that’s a sudden job loss, a medical emergency, or an unexpected major expense.

This fund provides a cushion of money that can keep you afloat during challenging times without needing to borrow or take on more debt. It brings peace of mind, knowing that you have resources to lean on when life goes awry. In the context of our quest to become debt-free, an emergency fund is invaluable—it helps you stay on course even when faced with sudden financial hurdles.

How Much to Save: Tailoring Your Safety Net

Determining the size of your emergency fund isn’t a random guess—it’s a balance between your monthly expenses and your peace of mind. A general rule of thumb is to save enough to cover three to six months’ worth of living expenses. This includes rent or mortgage payments, groceries, utilities, transportation costs, and any other recurring bills.

However, this is not a one-size-fits-all scenario. The right amount for you depends on your individual circumstances. If you have dependents, or if your income is irregular, you might want to aim for a larger safety net. In contrast, if you have good health insurance, low fixed costs, or a high, stable income, you might be comfortable with a smaller fund.

The trick is to start small if necessary, and then build gradually. Even a modest emergency fund can provide a measure of security. Regularly set aside a percentage of your income until you reach your goal. This practice not only builds your emergency fund but also cultivates a habit of saving—a skill that’s priceless in your journey to becoming debt-free by age 30.

As we brace for the unexpected with our emergency fund, let’s venture forth to the final rule.

Rule 4: Invest in Yourself

Often when we think of investing, our minds leap to the stock market, real estate, or other similar avenues. While these are vital, there’s one crucial investment that deserves your attention – investing in yourself. This rule isn’t just about boosting your financial strength—it’s about fostering personal growth and increasing your potential for wealth generation.

Importance of Continued Education: Your Knowledge, Your Asset

In today’s ever-evolving world, staying abreast with new skills and knowledge is indispensable. Not only can this improve your job prospects and earning potential, but it also provides a sense of fulfillment and confidence that is priceless. This could mean undertaking further formal education, enrolling in online courses, attending seminars, or even reading widely to stay informed.

However, investing in your education isn’t just about developing hard skills like programming or digital marketing. It’s also about cultivating soft skills like communication, leadership, and emotional intelligence, which can be just as valuable in the workplace. Think of it this way: every new skill or piece of knowledge you acquire is a tool in your toolbox, giving you an edge in your career and ultimately increasing your capacity to earn—and save.

Investment Opportunities: Your Path to Long-term Wealth

While paying off debt is a vital step towards financial freedom, creating wealth is equally important. Once you’ve managed to clear your debts and establish your emergency fund, consider stepping into the world of investing.

There’s a wide range of investment options available, each with its own potential returns and risks. These include stocks, bonds, mutual funds, real estate, or even starting your own business. Investing allows your money to grow over time, potentially leading to long-term financial stability and independence.

Remember, investing is not about getting rich quickly; it’s about consistent growth over time. It’s crucial to do your research, perhaps seek advice from a financial advisor, and choose investments that align with your financial goals and risk tolerance.

There’s no denying that navigating the world of finance can be daunting. However, with a little bit of knowledge, discipline, and patience, becoming debt-free by 30 is an achievable goal. The journey to financial independence is a marathon, not a sprint. Stay the course, and you’ll reap the rewards.

Related: 4 Ways To Stay Positive While Paying Off Debt >>

Conclusion: Chart Your Path Towards Financial Freedom

As we come to the close of this roadmap to debt-freedom by 30, let’s revisit the essential rules we’ve unpacked.

- Cultivate a Healthy Relationship With Money: Understand money as a tool, rather than a panacea. Embrace the discipline of budgeting and the empowerment of living within your means.

- Prioritize Debt Repayment: Comprehend the impact of debt on your financial health and personal well-being. Strategize your repayment with proven techniques, taking decisive steps towards a debt-free life.

- Build and Maintain an Emergency Fund: Recognize the security that a well-cushioned emergency fund provides. Determine the right size for your safety net based on your unique needs and circumstances.

- Invest in Yourself: Realize the power of knowledge and continued learning in escalating your earning potential. Uncover diverse investment opportunities for long-term wealth generation.

By integrating these four rules into your financial strategy, you’ll be setting strong foundations for a debt-free future.

But remember, change begins with a single step. It’s about making that initial commitment and then sticking with it, step by step, day by day. Your financial freedom journey starts with you – with that first decision, that first dollar saved, that first debt repaid.

So, why wait? Start today, and seize control of your financial future. Let’s celebrate the prospect of a debt-free, financially empowered future by taking those crucial first steps today. After all, the journey to financial freedom isn’t just about the destination—it’s about growing and learning along the way.